Selling Options Premium for Consistent Income: The Complete Framework

Selling Options Premium for Consistent Income: The Complete Framework

Selling options premium is one of the most systematically profitable strategies available to retail traders — when executed with discipline. The core logic is elegant: options buyers pay you today for the possibility of a future event. When that event doesn't materialize, time erodes the option's value and that decay becomes your income. Theta works for you the way gravity works — constantly, quietly, and without sentiment.

Selling options premium is one of the most systematically profitable strategies available to retail traders — when executed with discipline. The core logic is elegant: options buyers pay you today for the possibility of a future event. When that event doesn't materialize, time erodes the option's value and that decay becomes your income. Theta works for you the way gravity works — constantly, quietly, and without sentiment.

But premium selling is not passive income. It is a defined process with non-negotiable prerequisites. What separates consistent theta farmers from retail casualties is a rigorous pre-trade checklist and ironclad position management. This post lays out that complete framework — the questions, the mechanics, and the tools — so you can approach every trade with the discipline of a professional market maker.

Why Selling Premium Works: The Volatility Risk Premium

Before the how, the why. Options sellers have a persistent, empirically documented edge called the volatility risk premium (VRP): implied volatility (IV) — the market's forecast of future movement — consistently overstates actual realized volatility in most underlyings, most of the time.

The implication is structural: if you consistently sell IV that is priced higher than what actually occurs, you collect more premium than the moves justify. This isn't a guarantee on any single trade. It is a probabilistic edge that compounds over hundreds of trades — which is why position sizing and frequency matter as much as trade selection.

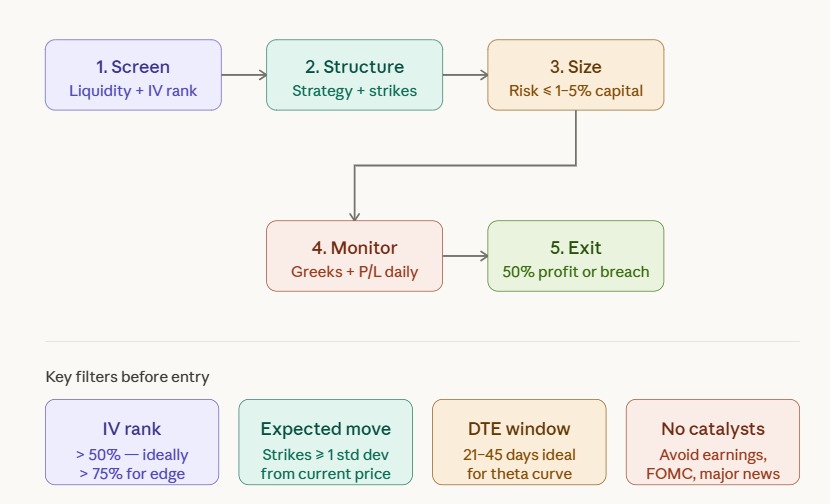

The Pre-Trade Framework: Five Non-Negotiable Questions

1. Which underlying should you sell premium on?

Not all tickers are created equal for premium selling. Your ideal underlying has:

- Deep liquidity — bid-ask spreads under $0.05 on the options, millions of contracts in open interest, billions in daily equity volume. SPX, SPY, QQQ, and top single-name equities (NVDA, AAPL, TSLA) dominate for a reason.

- No imminent binary events — a single earnings release or FDA decision can gap a stock 20-40% overnight, obliterating a premium selling position in minutes.

- Sufficient IV to justify the trade — you need enough premium to cover transaction costs, margin requirements, and still leave a meaningful return.

ETFs and indexes are generally safer for consistent premium selling because they don't gap on individual company news and carry better margin treatment. Single names offer higher premiums but introduce event risk that must be managed carefully.

2. Is IV elevated relative to its own history?

This is the most commonly skipped step, and skipping it is why most retail premium sellers underperform.

IV rank tells you where current IV sits relative to its own 52-week range. An IV rank of 80% means IV is higher today than it was 80% of the time over the past year. IV percentile tells you what percentage of days over the past year had lower IV than today.

Selling premium when IV rank is below 30% is like selling fire insurance in winter — you're collecting small premiums but absorbing all the downside exposure if volatility spikes. The edge disappears.

Target IV rank ≥ 50% as a minimum. IV rank ≥ 75% for high-conviction trades. High IV environments occur naturally around earnings cycles, macro events, and volatility shocks — and they represent your best opportunities, provided the catalyst itself has passed and you're positioned for mean reversion.

3. What strikes should you sell, and how wide should the spread be?

Strike selection flows directly from expected move calculation. Using IV, you can estimate the one-standard-deviation expected move over any given timeframe:

Expected Move ≈ Underlying Price × IV × √(DTE/365)

A position placed one standard deviation out-of-the-money (OTM) carries approximately a 68% probability of expiring worthless — meaning you profit roughly 68% of the time before any active management. Two standard deviations out gives approximately 95% probability, but the premium collected shrinks dramatically.

The practical sweet spot for most premium sellers sits between 0.8 and 1.2 standard deviations from the current price — far enough to win most of the time, close enough to collect meaningful premium.

For spread width: wider spreads (e.g., $10-wide iron condors vs. $5-wide) collect more gross credit but face proportionally larger losses on breach. Narrower spreads require you to be right more often. The decision depends on your risk tolerance and how aggressively you're willing to manage positions.

4. What is the optimal time to expiration?

Theta — the daily rate of time decay — is not linear. It accelerates dramatically in the final weeks before expiration, following a curve that steepens around 21 days to expiration (DTE) and becomes exponential inside 7 DTE.

The 21-45 DTE window is the professional standard for theta-selling entries. You enter when decay is already accelerating but gamma risk (the rate at which your delta exposure changes with price movement) hasn't yet become dangerous. Many systematic sellers target closing positions at 21 DTE — capturing the bulk of the theta decay while cutting gamma exposure before it becomes unmanageable.

Very short-dated trades (0-7 DTE, popularized as "0DTE") collect rapid theta but carry extreme gamma risk — small moves can create disproportionately large losses. These require constant monitoring and are appropriate only for experienced traders with clear adjustment protocols.

5. What is your exit plan before you enter?

Amateur traders think about exits after a trade goes wrong. Professional sellers define their exit rules before they enter — and follow them mechanically.

The industry standard for profitable premium selling management:

- Take profit at 50% of max credit received. Research from platform data consistently shows that closing at 50% profit dramatically improves risk-adjusted returns versus holding to expiration — you capture most of the available theta while avoiding the gamma risk of the final weeks.

- Close or roll when the position reaches 200% of credit received as a loss. Defined-risk spreads already cap your max loss; undefined-risk positions (strangles, naked puts) require this discipline even more urgently.

- Roll threatened positions before breach, not after. Rolling involves buying back the current expiration at a debit and re-selling a further expiration for credit — defending the position while maintaining the theta-collecting structure.

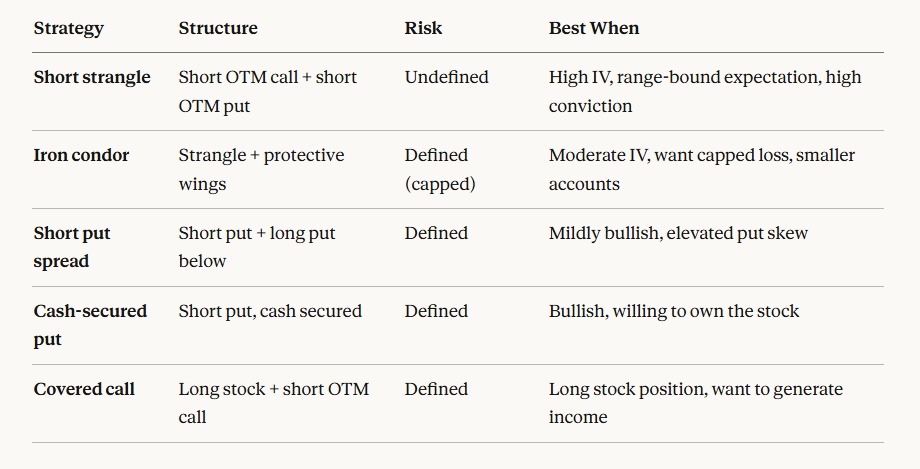

Choosing the Right Strategy

The "right" structure depends on your market outlook, risk tolerance, and whether you want defined or undefined risk:

The defining question is always: are you willing to accept unlimited (or large) losses in exchange for higher premium, or do you prefer a capped-loss structure at reduced premium? Neither is wrong — but the answer must be consistent with your account size and emotional discipline.

The defining question is always: are you willing to accept unlimited (or large) losses in exchange for higher premium, or do you prefer a capped-loss structure at reduced premium? Neither is wrong — but the answer must be consistent with your account size and emotional discipline.

The Greeks You Must Understand as a Seller

Selling premium means you own a specific Greeks profile by default. Understanding it is not optional:

- Theta (Θ): Positive for sellers — you earn daily decay as long as price stays in range.

- Delta (Δ): Near-zero for neutral strategies (iron condors, strangles). Positive for short puts. Directional bias shows up here.

- Vega (V): Negative for all premium sellers — you lose money if IV rises after entry. This is your primary risk in a vol spike.

- Gamma (Γ): Negative — a large price move against you accelerates losses. Gamma risk intensifies dramatically inside 14 DTE.

Managing a premium selling portfolio means monitoring these continuously. A position that starts delta-neutral can become significantly directional after a 3% move in the underlying. Staying aware of your live Greeks — especially delta drift and vega exposure — is the difference between an active manager and a passive lottery ticket holder.

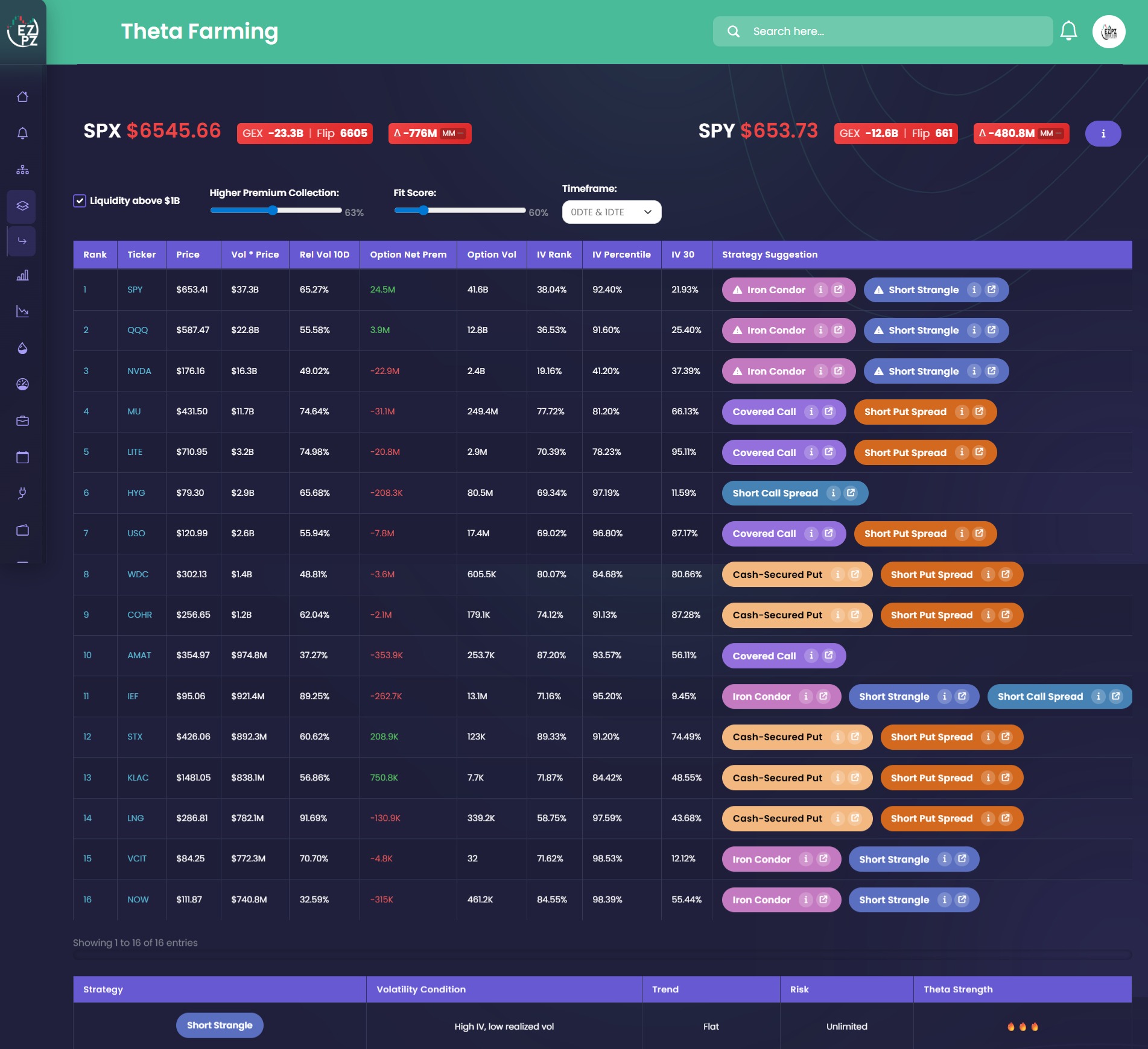

The EZPZ Theta Farming Edge

Answering all of the above questions manually — across dozens of potential underlyings, in real time, with current data — is practically impossible without specialized tooling. You'd need to pull IV rank data, calculate expected moves, screen for liquidity, filter for catalyst risk, and compare premium across expirations for every candidate. By the time you've done it manually, the opportunity has moved.

That's exactly what the EZPZ Theta Farming pages are built to solve.

Our platform runs a 20-point systematic inspection across every eligible ticker in real time. The output is a ranked leaderboard of premium-selling opportunities, filtered for true edge: high IV rank, sufficient liquidity, clean catalyst windows, and favorable Greeks structure. For each top candidate, EZPZ auto-suggests the optimal strategy and delivers ready-to-trade setups across three timeframes:

- Short-term — rapid theta collection, high gamma awareness

- Weekly — balanced theta/gamma, the most popular timeframe for consistent income

- Monthly — larger premium cushion, steadier but slower decay

Every setup includes a full Greeks breakdown, precise breakeven points, net credit received, and a real-time interactive P/L heat map showing your profit or loss at every possible price level from now to expiration. You see your risk before you take it — not after.

This is the analysis institutional market makers run internally, now available to retail traders with a few clicks.

The Bottom Line

Selling options premium works because implied volatility persistently overestimates realized volatility, and because time decay is relentless. But the edge is only captured by traders who execute systematically: screening for IV rank, placing strikes at defensible distances, sizing positions conservatively, managing Greeks actively, and exiting at predefined profit targets.

Every shortcut in this process is a risk you're taking invisibly. Every step you execute correctly compounds over time into a genuine, repeatable edge.